- Arbitrage. With perfect foresight and no risk premium the return one-year bond should be equal to the interest rate on a six-month bond bought today, reinvested in a six-month bond bought six months from now. (1+i1)(1+i2)=(1+yr) reflects compounding. Now rates are quoted as one-year rates, so if the six-month rate is quoted as 0.6% then the actual return is (1+x)(1+x)=1.006 so sqrt(1.006)=(1+x)=1.0029955 or 1.003. That is, half the one-year rate is a very close approximation when rates are low. So if the one year rate is 1.0082, then the implied return for the second six months is 1.0083/1.003 = 1.0052. That is, markets expect the 6-month interest rate six months from now to be 1.04%. In other words, the FOMC will continue boosting rates at a steady pace.

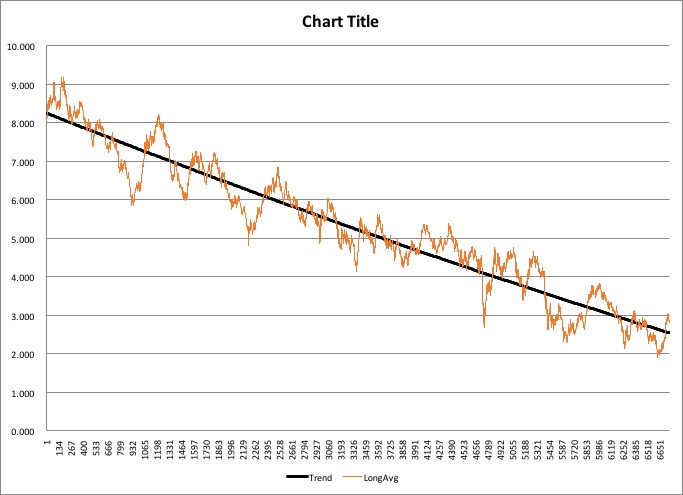

- Here is what has happened since 1990 to long rates. I used the average of 20-year and 30-year bond rates, in part because there are years in which only one or the other was available. Just to check, I downloaded the excel spreadsheet as an .xml file (Excel 2004 format), imported into Stata, and regressed interest rate = constant + a*date + b*date2. That’s the trend line in the graph. (I forgot to convert the date sequence to give the proper x-axis labels. The series starts Jan 2, 1990 and runs to yesterday.)

- I also calculated the implied yield on long bonds, using the same approach as in (1) above, by comparing the yields on 7 year bonds and 10 year bonds, and 20 year bonds versus 30 year bonds. That graph shows that markets have built in somewhat higher yields.

- Is it sensible that over the next 30 years inflation will never top 2%? In other words, if I were to factor in a risk premium, what would change?

- Back out from that what markets “believe” growth will be 20-odd years from now.

- What questions does that raise? (Many, I trust!)

For your reference I’ve written about this on Autos and Economics.

5 Comments

If 1-yr bonds currently yield about 0.5% (based on the graph), and 30 yr. bonds are yielding about 3%, we can reasonably assume that we will achieve inflation of 2% over that 30-year time period. The market indicates that inflation is expected to be 2.5%, the differential between 30 yr. and 1 yr. rates. This proposition is sensible. However, the yields of 30 yr. bonds are only representative of the expected net change in the inflation level in exactly thirty years’ time. It is at best an assumption, and the market, though usually an effective judge, cannot predict the occurrence of a future event which might disrupt the status-quo. These expectations can instantaneously change with the occurrence of such an event. It is also interesting to look at the average of 20 yr. and 30 yr. rates. They are notably higher than 7 yr. rates, at about 3.5%, but also higher than the expected 30 yr. rate. It would follow that average inflation is expected to be around 3% in the span of 20 to 30 years from now. Does this suggest a period of high inflation is expected over the next twenty years (possibly 4%), but followed by a period of lower inflation after that, representing a sort of regression to the long-run natural rate of inflation? This raises questions about the existence of a natural rate of inflation, and the market’s expectations of inflation to gravitate around such a level. It also displays confidence that the economy will not remain stagnated at its current plateau.

Good, we’ll do more calculations, try to make this precise. But remember that you should be able to earn a return in many different ways that is equal to the nominal growth rate of the economy. So we should be looking at (real) growth plus inflation, not just inflation.

It is not necessarily accurate to assume that over the next 30 years, inflation will never top 2%. In the graphs, it is evident that though there is a general trend over the years, there are spikes and drops through specific years probably due to various factors, and that the predicted inflation rates are not always correct because the economy is constantly changing. As a result, inflation never topping 2% is not a guarantee though inflation could generally be predicted to be around 2% over the next 30 years. Whether or not it is sensible depends on how confident we are that the market will react the way we estimate it will. If risk premiums were included in the analysis, then the real return on the bonds would not equal the nominal interest rate. For example, the return on a one-year bond would not be equal to the interest rate on a six-month bond bought today that is reinvested for six-months (See equations above). While markets expect the interest rates to be a specific number, the federal open market committee often can interfere to alter the rates in order to match expectations and determine what direction monetary policy follows. In conclusion, including risk premiums in inflation analysis show that the real return on bonds could be different than what is expected. As a result, including this number in the analysis would alter the outcomes that we predict to see. However, one question I have is, how different would it be if the risk premiums were included? Additionally, it is interesting to note that there is usually not perfect foresight of the events that will occur in the future that may impact the prediction of the models that we have. As a result, it is hard to say what inflation will be with complete certainty in thirty-year time.

I would be surprised if inflation does not top 2% over the next thirty years. Even though we currently live in a low interest rate and low risk environment the thirty year rate reflects the level of risk associated with the current moment in time. As previously stated, the FOMC often interferes with the interest rate in order to match expectation and this morning (1/12/17) Philadelphia Fed President Harker said that with the considerable strength in the economy he expects 3 rate hikes. I would think that with the recent changes in government the risk profile of the world would increase due to general policy uncertainty. As tensions increase as well in Latin America and the Middle East, risk premiums will continue to increase and lead us back to a path of “normalcy” that may even exceed expected inflation of 2%. In addition to increases in global risk, I believe that the current technological revolution will also bring about an age in higher investment. While the technology revolution of the 90’s has all but ended, there is a new era in “smart” technology that can potentially revolution the consumer economy by meeting all demands before they are made clear. In addition to that, the advances in robot technology will cease the necessity for menial labor and allow for re-investment not only in infrastructure/education but of job creation in fields we don’t currently have the capability for which will help boost the economy above the currently predicted 2% inflation level.

Good. A complicated topic, but until you start puzzling things out yourself, the “why” of various steps won’t make as much sense.

Guidance: yield today = 3% = expected inflation + real economic growth + risk premium. Why add the latter? Holding a 30-year bond opens you to the potential of more shocks than holding a 20-year bond, and so on. So for any given level of interest rates you need to be paid more to bear greater risk. In fact Friday the yield on the 30-year bond was 2.99%, that on the 20-year was 2.71% or a 28bp difference (1 basis point = .01 percentage points). However, when I looked at the data it was odd: during a period of several years 30-year bonds actually paid less than 20-year bonds. That was never true for 20-year vs 10-year bonds. (OK, there were 7 days in 2000 when that happened – excel has a “countif” function, no easy way to eyeball 6000+ data points!)

So … 30-year bonds may be idiosyncratic, held for reasons that don’t lead to arbitrage against shorter maturities. A spot-check (20 year bonds above) suggests that at longer maturities it’s only 30-year bonds that look odd.

Back to risk premia: the average difference between 20- and 30-year bonds is 3 bp, between 10- and 20-year bonds it’s 55bp and between 5- and 10-year bonds it’s 58bp.

That doesn’t get us around the dilemma: 20-year rates have been less than 3% since October 2014. If we subtract 50 bp as a risk premium, then we have 2.5% = inflation + growth. Even if we assume that the risk premium has fallen, we still have interest rates building in future growth at less than 1.5%, and under 1% if we peg inflation plus the risk premium at 2%.

https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield

Comments are closed.