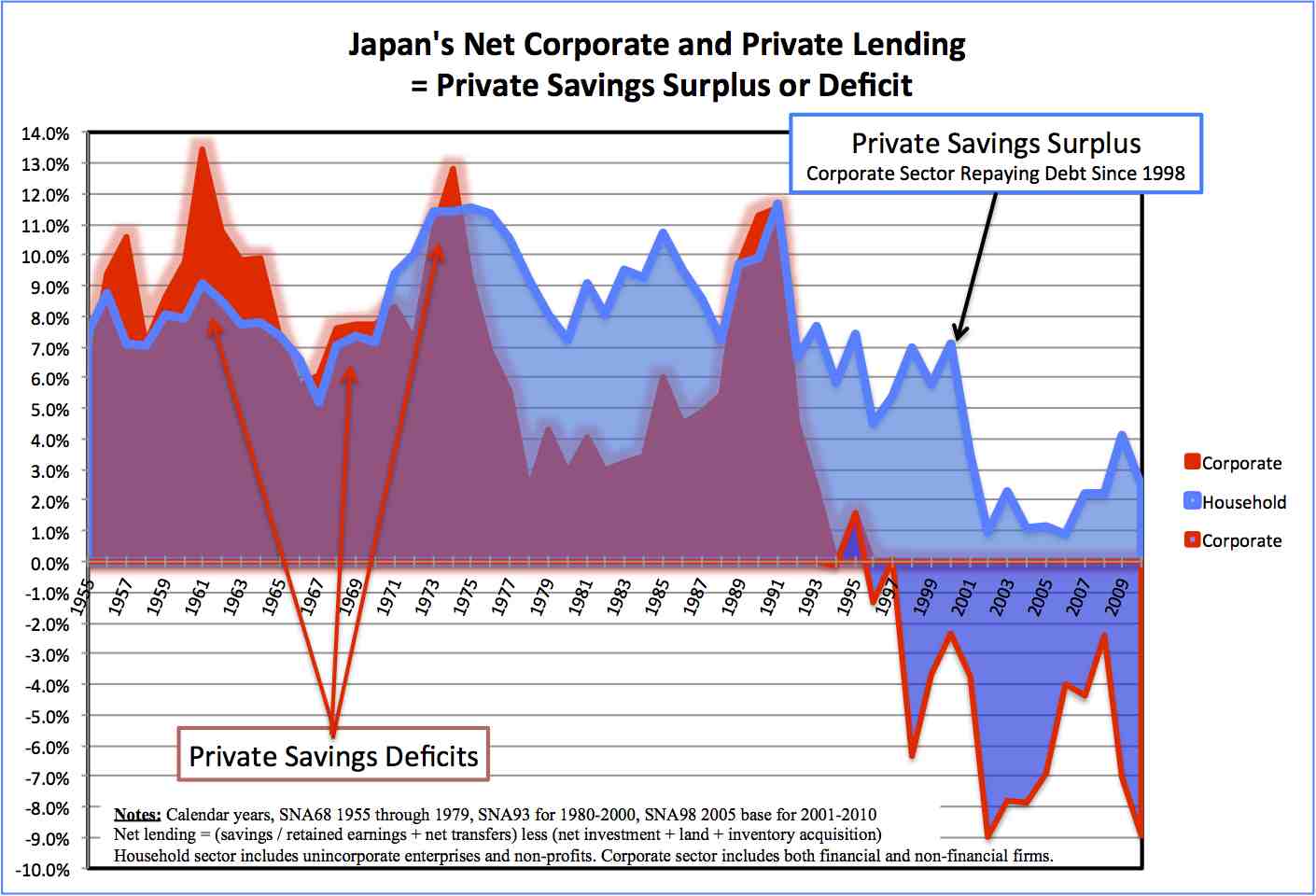

Japanese data on corporate and private savings highlight two things. The first, and here but an aside, is the tendency of the economy towards an excess of private savings since 1970. Tracing the outworkings of that provides one way to organize what has happened to Japan’s macroeconomy over the past 40 years, great for the economics classroom. But that story is not for here.

Rather, I want to point out the magnitude and duration of deleveraging following the 1991 collapse of Japan’s real estate bubble. Unlike in the US, Japan’s bubble was driven by corporate borrowing; households were actually net sellers of real estate, particularly land. And so in Japan’s case it’s corporate deleveraging to which we need to look, the red line in the graph below. That’s gone on for 15 years, helping push the economy into a decade-plus of deflation despite the same global commodity price trends that affect the US and a huge run-up of the Bank of Japan’s monetary base.

This should be sobering, though I think the household vs corporate distinction matters. That’s because households want to be able to consume more, while corporations face no particular need to invest if they don’t think it will be profitable. So there’s no necessary tendency for a corporate savings surplus to end, US consumers would prefer to save less. Furthermore, adjustment in the US is helped by more aggressive foreclosures than occurred in Japan. Still, housing prices continue to decline, so while Americans have less debt, they also have less assets. So despite considerable deleveraging to date, the share of underwater mortgages remains around 25%.

I’m an example. My wife and I built our dream house, starting shortly after I returned in 2007 from a year in Japan. I hadn’t been following what was happening to the US economy…and hoped that Rockbridge County was sufficiently small and sufficiently attractive as a retirement haven to buck national trends. Wrong. As a consequence we still have our old house. While not underwater, I had planned on modest capital gains from selling it to help pay down the costs of our new house. So now I have a lot more debt than intended, and less cash flow. I definitely am holding back consumption as I deleverage. In the aggregate I and tens of millions in similar positions constitute a drag on growth, and on job creation.

How long will deleveraging continue? I’ve not tried to crunch numbers; I would want data not just on how many mortgages are underwater, but by how much broken down by quartiles. Not today! My gut feeling, hardly reliable, is that we’ll need two years after housing prices stabilize for deleveraging to work its charm and consumption to recover. (Overbuilt retirement havens such as Las Vegas may take longer…) But – yikes – housing prices are still falling. So if I’m to be consistent, that means I must believe growth will remain muted into 2014. It also means I fear deflation, not inflation. That’s for another post.

This graph draws from the System of National Accounts Yearbook for Japan; that for FY2010 is at long last out, Japanese GDP data unfortunately are not available very promptly and many subaccounts are only available on an annual basis. To create this chart, I spliced together than annual sectoral data from the three separate time series, as Japan changed its GDP compilation from SNA68 to SNA93, and then revised how it compiled SNA93. Because the underlying data needed to do consistent backward revisions are unavailable — the current SNA uses data that simply weren’t collected until 2001 — I did what I could, splicing together one series that goes from 1955-1998, another that goes from 1980-2009, and the current one from 2001-2010. Now macroeconomists are wont to pull their data from one or another warehouse (the Penn World Tables). Issues such as this mean I am in general skeptical of results from one statistical approach, that of cross-country regressions, which are plagued by such issues. More generally, it means I like to see the footnotes on data issues.