…age composition matters…

How long recovery takes depends on the rate of job creation relative to the growth of the working age population. It turns out that age composition matters. In 2005-6 the economy needed roughly 125,000 a month to keep unemployment from changing; by 2008, when the Great Recession began, that rate had fallen to 102,000. Continued shifts – more people at the retirement end of their working life – pull that down to 71,000 in 2012. It then drops to 65,000 in 2013-14 and 62,000 in 2015-16. Cumulated over 2008-2016 that’s a 5 million difference relative to the steady employment growth of the previous decade. (Addendum: Nowhere in the data does the shortfall get anywhere near the 23 million unemployed Romney repeated time and again in the second debate. He can’t be very concerned about the issue if, after 7 years on the campaign trail, he has no grasp of basic data.)

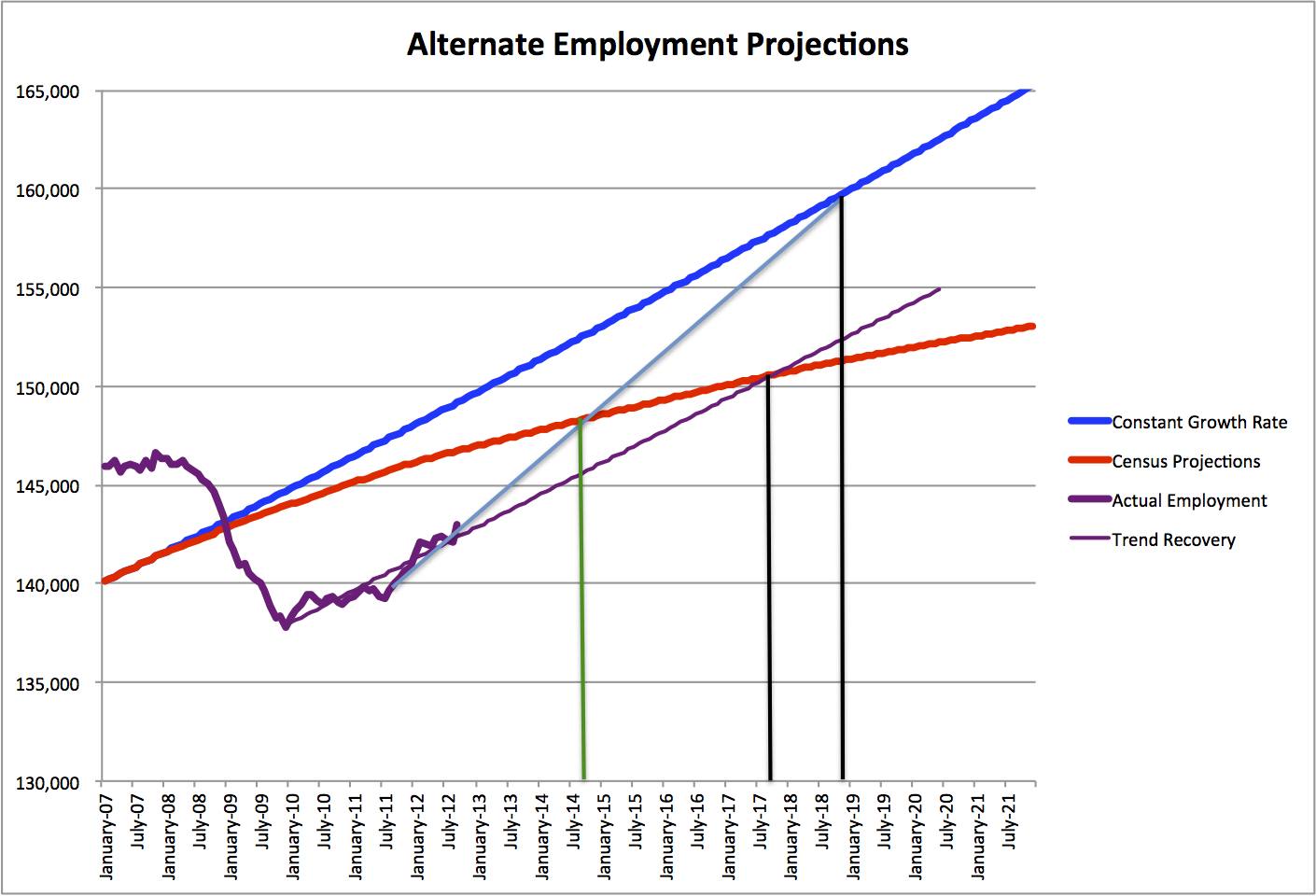

So first I calculated the expected normal level of employment, correcting for demographics; details are below the chart. I then calculated trend job growth (a simple regression using data from January 2010, the rough nadir of the recession, through Sept 2012). On that basis we return to normal levels of employment in fall 2018. If we naively take the faster average growth since summer 2011 (the light blue in the graph), we recover in time for the next midterm elections. That’s a sharp contrast to the naive straight-line projection of required employment growth, which doesn’t get us back on track until far into the future or (under the optimistic light blue scenario) late 2018.

I don’t believe the optimistic case – we face headwinds but no tailwinds. Congress can mishandle the Fiscal Cliff; global growth is slowing. For the latter, the Europeans have yet to provide Greece and Spain a politically viable strategy for staying in the Euro zone. China’s economy has slowed. Energy prices remain a drag, particularly on Japan which (due to the shutdown of most nuclear power generation) now faces a huge import bill for hydrocarbons. We are bit by bit moving out of the real estate bubble, as every quarter another 750,000 or so households will work out from being underwater on their mortgages, and as state and local government revenue stabilize. Nothing on the horizon will speed that process; neither presidential candidate has offered realistic proposals to address underlying issues.

Overall, however, this presents a far brighter picture than my previous calculations, which used the straight-line (blue) projections rather than the baby-boom-adjusted (red) projections. When I used the former, we were making almost no progress on closing the employment gap. But in fact we have made progress, even if it’s less than we’d like.

A bit of tedium on my calculations. I began by pulling employment to population data from the Bureau of Labor Statistics, a bit tedious as you have to pull a lot of data series, and the series include 13 observations per year because they include an annual number. So I had to delete those. (Thank you Nisus Writer, for making that easy!) Then I graphed it in Excel to see if the data suggested shortcuts.

As it happens, most of the employment-to-population data show no trend over the two decades prior to the onset of the Great Recession. You can observe the impact of increased schooling at the young end of the age spectrum, and a modest rise in the share of people working in older cohorts, those age 60 and above. Even in those cases, most of the shift was before 2005. If we go back further, there were larger changes in schooling and in women’s labor force participation, but those predate the 1990s. So with no trend going into the Great Recession – there is no upturn in the mid-2000s corresponding to the bubble – I could take the employment-population figures at the start of 2007 as the starting point.

I thus took the immediate pre-recession levels for 5-year age brackets, age 16-19, age 20-24 through age 70-74. (It would be wrong to stop at age 65, which is what most data sources do, because 18% of Americans are still working in their early 70s.) Note that in the Great Recession the share of people working fell sharply, particularly at younger ages (16-24) and among prime-age workers (those age 25-54). Hence for projections it’s necessary to use the (stable) prior level as the reference point. That doesn’t matter at older ages; the data show no wave of early retirement, if anything they show a very slight increase in labor force participation. (continued below graph…)

I then went to the US Census for population projections. The 2009 is the most recent, projection population by age for each year through 2050. I reduced these to the 5-year brackets used for the BLS employment-population data. To get the “normal” level of employment, I then multiplied the projected population in each 5-year bracket by the pre-recession employment-to-population ratio (for older workers, the most recent ratio) and added the totals. Since the Census doesn’t provide monthly projections, I simply took the annual increment and spread it evenly across each month.

Presumably sometime soon we’ll get projections based on the 2010 Census, but fertility rates change slowly, and even if the 2010 data are off, that will make a difference in the 16-19 age bracket only from 2026. Likewise, mortality was already very low in the age 60 bracket; the Census Bureau projects a continued drop in mortality, and that rate also changes slowly. So going out a decade won’t lead to much error there, either, and its impact is further reduced because employment rates drop. The weakest part of the projection is immigration. Since that presumably has fallen with our Great Recession, it means that if there’s an error, it’s towards an overestimate of the population and hence of the number of jobs our economy needs to create.

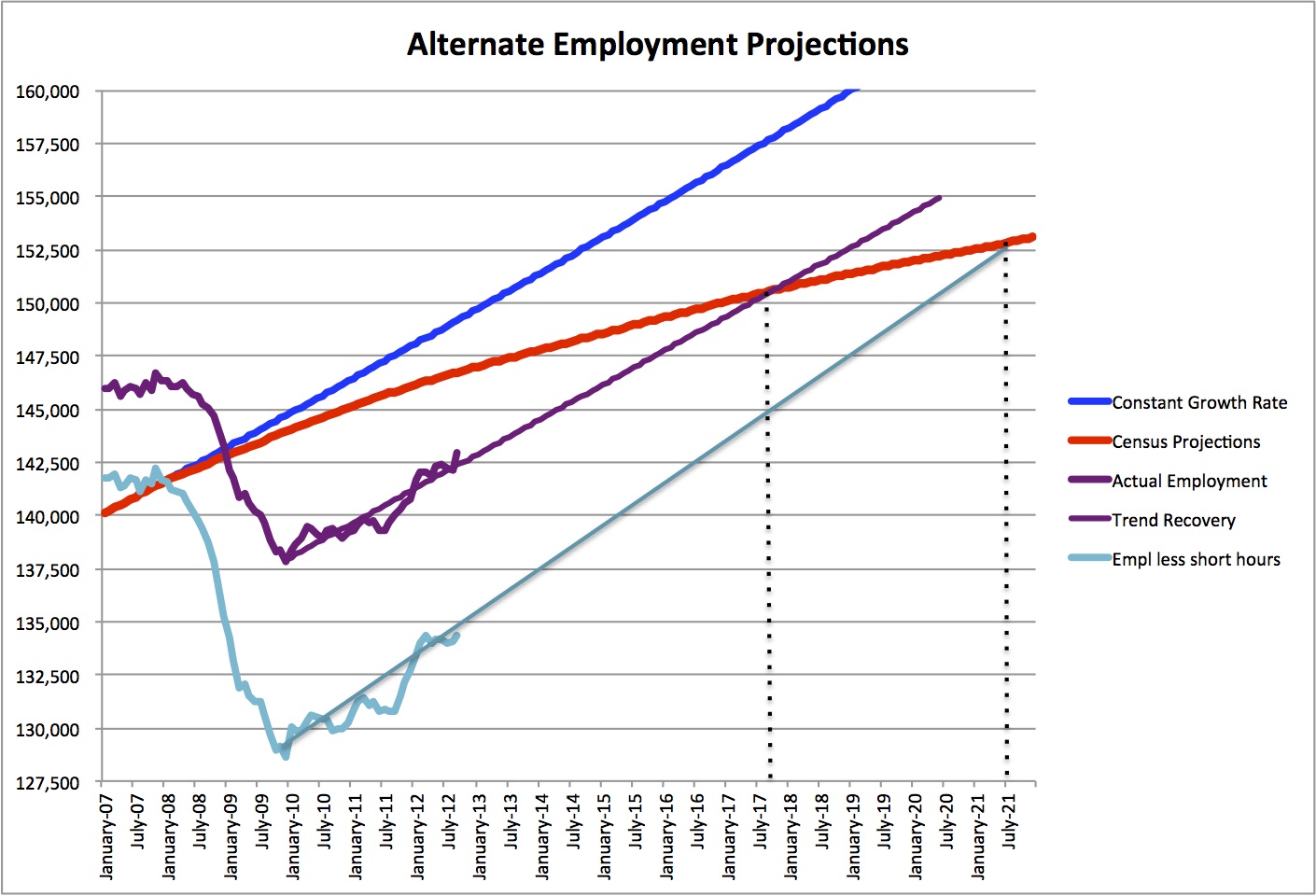

One final note is that these data are for employment, and not full-time employment. That means it does it take into account those working multiple jobs, and those working involuntary short hours. I cannot track either by age bracket. Glancing at the data suggests no particular trends in multiple jobs; in contrast, there has been a sharp rise in the number of those “working part-time jobs for economic reasons”. The latter means that I understate the amount of time recovery will take, because those jobs need to be converted back into regular jobs, on top of the need to create new jobs. Here’s what that graph does: it pushes the recovery date out past 2020…

…Mike Smitka…