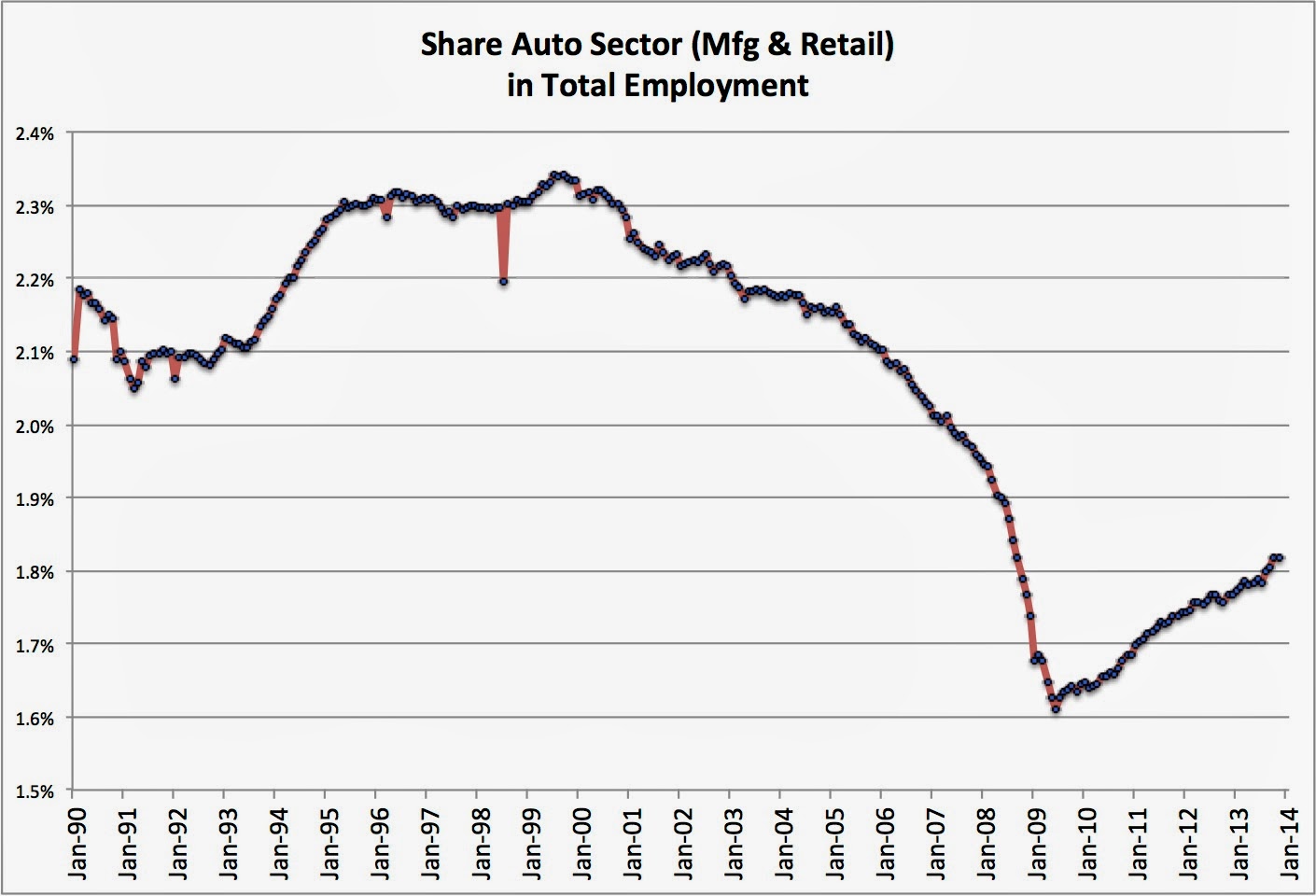

The US recovery continues at a snail’s pace; the auto industry is doing better. The rise in the SAAR [seasonally adjusted annual rate of sales] puts us below the bubble-inflated peak of 2005-6, but given subsequent population growth is at a more sustainable level. Other auto-related indicators show marked improvement, but suggest we still have a ways to go. First, the share of the auto industry (retail and manufacturing) was at 2.3% of the labor force in the late 1990s; it then fell steadily to 2.0% before falling off a cliff in 2008. The nadir was 1.6%; today we’re back to 1.8%. That is only about halfway, assuming that other structural changes in the US (the continued growth of healthcare) makes it possible to return to the days of yore.

…automotive employment’s only about halfway back…

If we look at the details, we get a more nuanced story. The retail side (which includes auto parts and not just vehicles) peaked at about 1.9 million workers; it fell by 300,000 during the Great Recession, and is now 2/3rds of the way back to that level. Manufacturing took a harder hit, falling from 1.1 million at the start of 2006 to 1.0 million in 2007, before dropping by 400,000 in 2008-9 to just above 600,000 workers or less than half the level of the late 1990s. We’re now back to almost 850,000, a sharper rise than in retail, but with further to go. Yes, suppliers are running at more than 100% capacity, and that must normalize. So employment will rise further, as overtime and other expedients are replaced by permanent hires. Still, it’s not clear that the US is on track to get back to earlier levels, though over the next few years other changes may help (e.g., Honda’s goal to export 30% of US-based production).

But overall the story from labor markets is of an anemic recovery. As the baby boomers retire, the growth of the working age population will slow. At present, however, we’re only just keeping up with population growth, and the gap between “normal” employment (I tracked age-specific levels back to 1994) is large, roughly 9.1 million workers as of November 2013. Furthermore, more jobs are part-time while a sizeable share of the labor force that had been working employed full-time are still working short hours. If we adjust for that, we’re shy 10.8 million full-time jobs. Let’s not forget long-term unemployment either, the 27+ week component is improving but is only down to what had been previously been the historic peak.

Finally, this is not due to boomers entering retirement early. Indeed, participation of older workers has trended up throughout the Great Recession and subsequent recovery. In other words, they aren’t retiring with past rapidity. That’s part of the reason that prime-aged participation rates remain below historic levels. Again, I’ve traced these levels back much futher – they were essentially flat going into the Great Recession. Now we can see a small increase since the worst of the recession, but only by about 1 percentage point to 95% of the previous norm. And the rate for young workers (age 20-24) remains in the abyss.

Click on the graphs to expand!

mike smitka