During the Federal Reserve stress tests last week, Goldman performed more poorly than other big banks. As a result, analysts and investors are showing concern that the bank may be barred by regulators from buying back its own stock, or increasing dividends. If this occurs, Goldman would lose a large component of their profitability. An analyst from KBW estimated that if Goldman is unable to repurchase shares, it could earn 42 cents a share less than expected this year, and $1.78 a share less than expected next year. Consequently, share of Goldman fell 1.7 percent on Friday, while the overall bank sector was up.

During the Federal Reserve stress tests last week, Goldman performed more poorly than other big banks. As a result, analysts and investors are showing concern that the bank may be barred by regulators from buying back its own stock, or increasing dividends. If this occurs, Goldman would lose a large component of their profitability. An analyst from KBW estimated that if Goldman is unable to repurchase shares, it could earn 42 cents a share less than expected this year, and $1.78 a share less than expected next year. Consequently, share of Goldman fell 1.7 percent on Friday, while the overall bank sector was up.

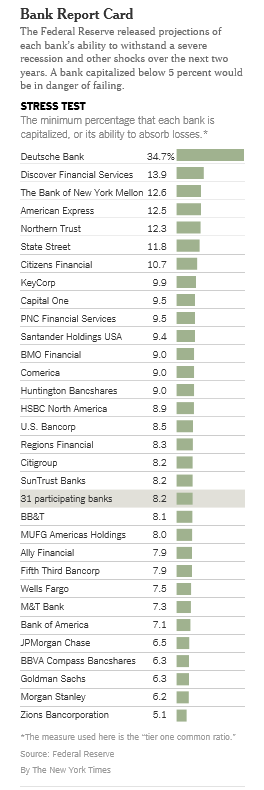

The stress tests are used to ensure that banks have adequate capital to sustain losses if another financial crisis was to occur. This year, the Fed measured how banks would do in a financial crisis if the stock market fell 60 percent, estimating that Goldman would lose $23.8 billion in its trading operations. The results of this stress test are in part due to the fact that Goldman has been returning a large share of its profits to its shareholders through buybacks and dividends, leaving it with less capital than it would have otherwise.

http://www.nytimes.com/2015/03/09/business/dealbook/at-goldman-sachs-stress-test-results-could-endanger-an-important-profit-source.html?_r=0

One Comment

Careful with the accounting: share repurchases don’t increase profits, only profits per remaining share – the opposite of “dilution”: new stock issues result in more shares but don’t change history, that is, booked profits, so profits per share (and ceteris paribus share price fall.

More important, this says that major US banks remain deeply embroiled in fee-generating businesses for which they fail to maintain adequate capital. Financial institutions devote teams of lawyers and “bankers” to devising new instruments, or at least ones new enough to not quite fit existing regulations. They are also deeply enmeshed in matters European. Boards of directors remain complicit: how can they leave in place executives who were in the line of command for malfeasance that incurred billions of dollars in fines?

Separately, wouldn’t it be better if corporations weren’t allowed to use profits to buy back their own shares, and instead could only use them to pay out dividends? Dividend payments are transparent, and all shareholders benefit. Share repurchases are not transparent, and for most shareholders the benefits exist only on paper, with no guarantee they can realize any profit even if they’re alert and careful. Dividend payouts would also lessen the ability of shareholders to dodge taxes. What I don’t know however is whether the amounts involved are large enough to have macroeconomic implications.

Addendum: Bank of New York Mellon is the US bank at the top of the list. They were one of only two major North American banks to maintain an AAA credit rating throughout the financial crisis (the other was ? Toronto Dominion). BNYM is a very interesting and quietly well-run institution. I don’t know how they are from a career standpoint; the downside of integrity may be job ladders that can only be climbed one step at a time.

Comments are closed.